Risikomanagement Journalistenakademie

|

|

|

- Käthe Arnold

- vor 8 Jahren

- Abrufe

Transkript

1 Risikomanagement Journalistenakademie Die Ungewissheit des Risikos Kann man in diesen Zeiten Risiko noch einschätzen und berechnen? Dr. Martin Rohmann 1

2 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 2

Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen")

3 Grundlagen Bankgeschäft Main function of banks is to act as intermediaries of fund transfers from liquidity providers (holders) towards liquidity buyers Banks within fund transfer activity are managing mismatch in tenor and currency of collected liquidity and demanded credit As intermediary service provider, the banks are taking the risk of debtors and protecting the creditors Main indicator of banks solvency is their capital, which can first absorb losses together with their profit 3

4 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 4

Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen")

5 ex post Was ist Risikomanagement? Risikomanagement ist die Identifikation, Messung und Steuerung von Risiko. RISIKOMANAGEMENT i.w.s RISIKOIDENTIFIKATION wo existieren Risiken welche Risiken gibt es wie kann ich sie messen RISIKOSTEUERUNG Organisationsform Kapitalallokation Risiko- / Ertragsoptimierung Risikolimitierung Diversifikation Ausbildung Hedging ex ante RISIKOCONTROLLING Quantifizierung Berichtswesen RISIKOMANAGEMENT i.e.s 5

6 How to Manage Credit Risk what is credit risk? example of a plain vanilla exposure debtor loan installments interest fees creditor (bank) Credit risk is a potential loss suffered by creditor by the reason that counterparty (debtor) is not able or willing to pay Credit risk is present in all kind of transactions where an exchange of funds takes place Elements of credit risk: counterparty risk, failure of debtor to meet financial obligations due to reasons related only to the debtor situation transfer risk, the risk that the debtor can not meet financial obligations due to reasons of restricted transfers (country moratorium of convertibility of exchange) settlement risk, failure within the settlement period of exchange of commodities 6

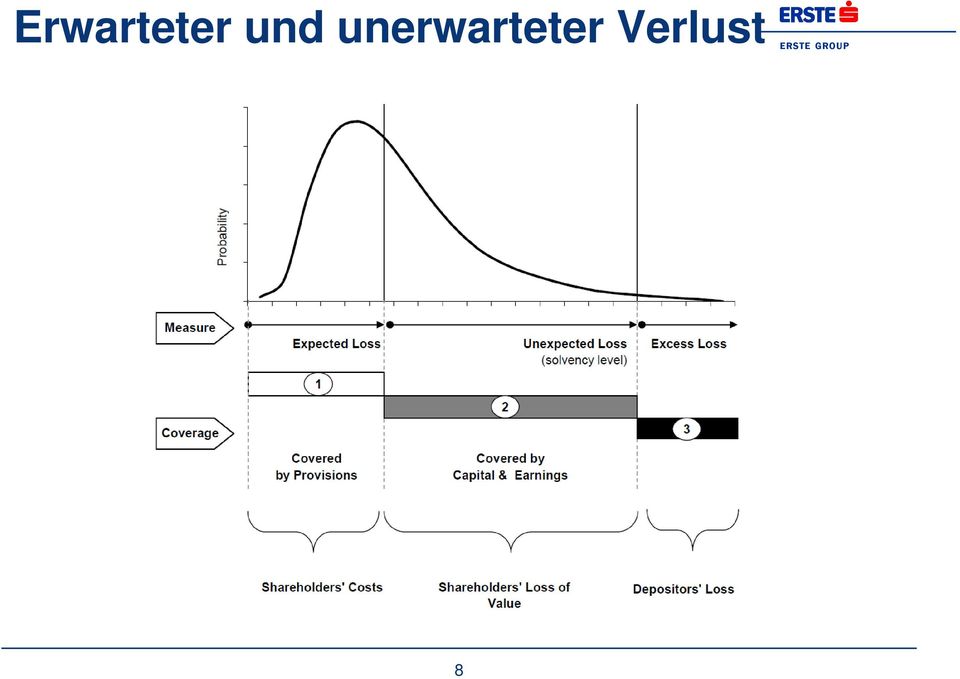

7 Erwarteter und unerwarteter Verlust Erwarteter Verlust Der Verlust, der im statistischen Mittel zu erwarten ist. Betrachtungshorizont: jährlich vs. (Rest-)Laufzeit des Kredites Muss durch risikogerechte Bepreisung verdient werden Standardrisikokosten Muss durch Wertberichtigungen bevorsorgt werden Risikovorsorgen Unerwarteter Verlust Der Verlust, der über den erwarteten Verlust hinausgehen kann. Wird mit einer gewissen statistischen Wahrscheinlichkeit (z.b.: 99.9%) ermittelt. Betrachtungshorizont: üblicherweise 1 Jahr Wird durch die RWAs berechnet Muss durch Eigenkapital abgedeckt werden können Die notwendigen Kapitalkosten müssen verdient werden 7

ermittelt.")

8 Erwarteter und unerwarteter Verlust 8

9 Empirie vs. Schätzung Historische Ausfallund Verlusterfahrung Prognose der PD, LGD, CCF (EAD) Vergangenheit beobachtet Heute Zukunft erwartet Ausfälle: 1 Jahres PD 1 Jahres Ausfallraten, Anzahl der je Ratingmethode und Ratingklasse Ausfälle und Ratingmigrationen Tilgungen: Tilgungsquotient Tilgungsquote je ausge- je homogenem Segment fallenem und abschlossenem Kunden Sicherheitenerlöse: Sicherheitenerlösquotient Sicherheitenerlösquote je je homogenem Segment vollverwerteter Sicherheit Off-Balance-Ausnützung: CCF Ausnützungsquote des freien je homogenem Segment Rahmens je ausgefallenem Konto LGD 9

10 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 10

Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen")

11 Die Verlustausgleichsfunktion des Eigenkapitals Eigenkapital ist ein Puffer gegen zukünftige, auch sehr unwahrscheinliche, unerwartete Verluste und muss überdies sicherstellen, dass das notwendige oder angestrebte Kapazitätsniveau notwendiges aufrecht erhalten Mindestkapital Performancemessung werden kann. Risiko Kapital Risikotragfähigkeit 11

12 Die Einflussfaktoren auf die Höhe des Eigenkapitals Risiko Regulatorische Vorschriften Eigentümer Markt Die Höhe des Eigenkapitals 12

13 RWA Kurve Sensitivity of Risk Weights to PDs (unsecured) 200% 180% 160% 140% 120% 100% 80% Risk Weighting CORPORATE SME Potential capital relief for retail 60% 40% OTHER RETAIL 20% PDs 0% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00% main Corporate PD area main SME PD area main retail PD area 13

14 A Within the IRB approach, different formulae are applied to different portfolios The value of Asset Value Correlation (AVC) factor/function has a large impact on the risk weights (all other parameters being equal) AVC and risk weight as a function of PD (LGD=45%, M=2.5 years *) ) in the IRB Approach according to Basel II Sovereign, Institute, Corporate SME Corporate (Firm Size 5 mio EUR) Retail Other Retail Mortgage Retail Qualified Revolving Retail STD-Approach Corporate STD-Approach IRB approach Asset Value Correlation Basel II risk weights 24% 300% 22% 275% 20% 250% 18% 225% 16% 200% 14% 175% AVC 12% RW 150% 10% 125% 8% 100% 6% 75% 4% 50% 2% 25% 0% 0% 5% 10% 15% 20% 25% 30% PD *) M parameter in the Basel II formula exists only for non-retail portfolios 14 0% 0% 5% 10% 15% 20% 25% 30% PD

PDs portfolio mix Others Retail other (revolving,")

15 D Pronounced differences in Risk Weights of different Banks Retail Mortgages: Possible drivers for relative differences are: LGD input parameters (house prices, ) State guarantees (e.g. in France) PDs portfolio mix Others Retail other (revolving, SME): 15

PDs portfolio mix Others Retail other (revolving,")

16 Qualität Eigenmittel (Total Capital, TC) hartes Kernkapital (Common Equity Tier 1, CET1) = Grund- und Stammkapital + einbehaltene Gewinne anderes Kernkapital = Hybridkapital NEU Kernkapital (Tier 1, T1) Ergänzungskapital NEU (Tier 2, T2) nachrangiges Kapital (lower Tier 2) 16

Ergänzungskapital NEU (Tier 2, T2) nachrangiges Kapital (lower")

17 Quantität heute Basel III 2019 min Basel III 2019 max Aufsichts-Add-On? SIFI-Surcharge? T2 (2%) T2 (2%) T1 (1,5%) Total:?? T1 (1,5%) antizyklischer Puffer (0-2,5%) Total: 8 % T2 (4%) T1 (2%) Total: 10,5 % Konservierungspuffer (2,5%) CET1 (4,5%) CET1: 7% Konservierungspuffer (2,5%) CET1 (4,5%) CET1 : 9,5% oder höher CET1 (2%) CET1: 2% 17

CET1 (4,5%) CET1: 7% Konservierungspuffer (2,5%) CET1")

18 Basel III zusätzlicher Kapitalbedarf in Mrd EUR Zusätzlicher Kapitalbedarf der AT Banken unter Basel III Mrd. EUR 4 Mrd EUR max. 3 Mrd EUR 4 6 Mrd EUR Mrd EUR CET1 strengere Basel III Anforderungen CET1 Ersatz staatliches und privates Partizipationskapital Additional Tier 1 Tier 2 Der zusätzliche Kapitalbedarf für den AT Bankensektor beläuft sich auf Mrd EUR Annahmen: -Der Kapitalbedarf beinhaltet Common Equity Tier 1, Additional Tier 1 und Tier 2 Kapital -Der Kapitalbedarf wurde auf Basis Q nach allen Übergangsbestimmungen (Definition per 2022) berechnet. -Es wurden keine Gewinnthesaurierungen und keine Ersatzbeschaffung für das staatliche Partizipationskapital berücksichtigt 18 Quelle: OeNB

berechnet.")

19 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 19

Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen")

20 Mögliche Reaktionen auf Kapitalknappheit Erhöhung Eigenkapital Kürzung Dividendenauszahlung Erhöhung Gewinn / Reduktion Kosten Kapitalerhöhung Reduktion Risiko Abbau der Risikoposition Verkauf / Syndizierung bestehender Geschäfte Einschränkung Neugeschäft Verbesserung der Qualität des Risikos Strengere Bonitätskriterien bei Kreditvergabe Adäquate Risikobepreisung Verstärktes Einfordern von Sicherheiten Technische Optimierungen Optimierung der Rechenlogik im Rahmen der gesetzlichen Rahmenbedingungen Hebung der Datenqualität EB: Für Nicht- Kerngeschäft EB: Wichtigste Maßnahme 20

21 Capital Structure On track for timely EBA compliance EBA core tier 1 ratio at 31 Dec 11: 8.9% EBA capital gap narrowed to about EUR 166m, down from EUR 743 million Supported by 250m earnings in Q RWA decrease by a reduction of noncore business and technical effects Hybrid T1 and LT2 buyback to generate additional capital Approx. EUR 500m of hybrid T1 capital Approx. EUR 330m in lower tier 2 capital Positive capital impact of approx. EUR 200m Replacement with Basel 3 compliant Tier 2 instruments planned in 2012 Basel 2.5 (CRD III) CET 1 ratio at YE 2011 reaches 9.4%, exceeding the Basel II CT1 ratio of 9.2% at YE 2010 Core tier 1 ratio (total risk) = tier 1 capital excl. hybrid and after regulatory deductions divided by total RWA - including credit risk, market and operational risk % Core tier 1 ratio (total risk) 8.3% 9.2% 9.4% Dec 08 Dec 09 Dec 10 Dec % Core tier 1 ratio excl. part capital (total risk) 6.9% 7.7% 7.8% Dec 08 Dec 09 Dec 10 Dec 11

22 Impact of current regulatory reforms (IIF) Europe including CEE will be hit more severe with respect to growth and employments losses than the US, Japan or the Emerging Markets. Europe has the highest dependency ratio on banks Western Europe: 70% credit financed 30% bond financed CEE: over 85% credit financed US: 25% credit financed Requirements to adjust to the new capital and liquidity standards are the largest. Emerging markets: Many emerging economies have benefitted from infusion of foreign equity from mature economies. Basel III will significantly increase the costs of maintaining and increasing such emerging market presence for the foreign owners (as the cost of capital and funding is likely to increase in the home markets). Particularly challenging will be the liquidity requirements as domestic long-term bank funding markets are relatively thin. 22

23 Impact on SME financing Higher capital requirements force banks to build up their capital position by either capital increase and/or reduction of RWAs On average SME are relatively high-risk borrowers showing higher probabilities of default compared to sovereigns On average even strong capitalised SME have low or no external ratings due to their size SME depend more or less entirely on banks for external financing because their access to capital markets is limited Regulatory capital standards tend to overestimate the economic capital required in European retail banking (Basel II formulas) SME are more exposed to credit rationing and are hit first in times of credit rationing 23

24 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 24

25 A The special case of Sovereign Exposures (1/2) Standardised Approach Exposures to sovereigns are assigned a Risk Weight depending on the corresponding external OECD rating of the home country OECD-Rating Risk weight 0% 0% 20% 50% 100% 100% 100% 150% Exceptions: Exposures to Sovereigns in EU countries, which are denominated and funded in domestic or EU currency are assigned the risk weight of 0% (e.g. Greece in EUR) Exposures to Sovereigns in non-eu countries but with comparable supervisory regime, which are denominated and funded in domestic currency of the Sovereign are assigned the risk weight of 0% (e.g. Croatia in HRK) Current standardised risk weights of exposures denominated in EU-currencies: Austria, Czech Republic, Slovakia, Hungary, Romania, Croatia (in local currency), Portugal, Greece, Ireland, Spain Serbia Ukraine 0% 100% 150% 25

26 A The special case of Sovereign Exposures (2/2) IRB Approach Generally risk weights are calculated according to the supervisory formula using the parameters: PD internally estimated assigned depending on the internal rating grade LGD, M defined by regulator Exceptions applied in the Erste Group: Exception 1: EU law allows to apply the risk weight of 0% when the risk weight under Standardised Approach is also 0% Exception 2: Bilateral agreement with regulator to apply the risk weight of 0% to Sovereign exposures from Austria, Germany, Slovakia, Czech Republic, Hungary 26

27 Basics Banks have to fulfill LCR and NSFR as of 2015 and need to hold Highly Liquid Assets (HLAs). Assets are considered to be high quality liquid assets if they can be easily and immediately converted into cash at little or no loss of value. Narrow definition of liquid assets comprised of cash, central bank reserves and high quality sovereign paper, as well as a somewhat broader definition which could also include a proportion of high quality corporate bonds and/or covered bonds. at least 60% sovereign or supranational paper up to 40% corporates and covered bonds with 50% haircut It s very likely that in the final CRD IV the definition of HLAs will be softened, allowing also top securitisations and reducing the haircut for corporates. While for LCR calculation also foreign currency denominated paper would qualify, for Survival Period Analysis only ECB eligible paper (euro denominated) is relevant. 27

28 HLA definition There is no clear definition but the following principles shall offer some guidance: Low bid-ask spread Low credit and market risk Ease and certainty of valuation Low correlation with risky assets Active and sizeable market Presence of committed market makers (quotes always available) Low market concentration (diverse group of buyers and sellers) Flight to quality assets (historically) 28

29 The Polygon of Conflicting Targets 1) Not increase risk weights 8) Infrastructure for analysis and admin needed 2) Maximise income 7) Stick to euro denominated assets 3) Keep counterparty and market risk low 6) Excess liquidity in our home market currencies 4) Reduce cluster risk and avoid contagion effects 5) Stick to our core market strategy 29

30 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 30

31 Stress Tests Stress Tests required by regulator for internal risk steering: Governance Responsibility with management body (most senior / BoD; responsibility not only for ultimate results but also scenario design etc.) Integral to RM framework (e.g. consideration within ICAAP, includes all risk types and leverages knowledge from across the organization, proper staffing, processes & tools) Results shall be actively used for all kinds of management decisions (business strategy, limit framework, capital and funding strategy, risk mitigation management etc.) Methodology Sensitivities for specific portfolios or risks Comprehensive scenarios (risk types, regions, industries ) Exploitation of results Conclusions for capital, balance sheet and P&L Action management ICAAP ST integral to ICAAP with clear message for capital planning Clear link between risk appetite and strategy and stress tests 31

32 Generic Scenario Based Stress Test Stress Scenario (incl. trigger) Euro Zone Crisis a b Greece default Ireland default 2 + x default c Determination of the stress scenario Macro Economy (causal chains) Bank specific universe Banking Market Real Economy Markets (incl. Capital and Liquidity) Banking Book Trading Book P&L Credit Risk LLP, RWA Market Risk BB, TB, haircuts Sovereigns Haircuts, revaluation FIN LLP, revaluation Operational Risk AMA, OR loss P & L Interest, fee, trading Concentration Risk CR, inter-risk, P&L 32 GDP Unemployment Rate FX Rates Interest Rates Capital + liquidity sources / prices Business Strategy Capital Strategy Liquidity Strategy Definition of causal chains and resulting macroeconomic stress parameters Definition of stress parameters for the individual analysis areas of the institute (e.g. credit risk PD, LGD, CCF for regions, industries, customer groups)

33 Stress Testing Governance and Organization Supervisory Board Stress Test Expert Panel Strategic Risk Management Credit Risk Management Market Risk Management Operational Risk Management Liquidity Risk Management Asset Liability Management Economists / Research Group Performance Management Enterprise-wide Risk Management Credit Risk Holding Board (BoD) Market Risk OpRisk Liqui Risk P&L Executive Committees Holding Steering Group Clearly defined stress test process involves a variety of units and groups to exploit available skills and experience as best as possible Group policy for stress testing implemented Clear roles and responsibilities have been defined 33

34 Building blocks of bank-specific stress tests Definition of Macroeconomic Scenarios Translation and Computation Management Discussion and Results Qualification Integration into Steering Group Research and Economists provide macroeco status quo and outlook Stress Test Expert Panel discussion and Selection of stress scenarios Group Research and Economists provide macroeco parameters fitting with selected scenarios Additional definition of risk and P&L sensitivities Management discussion at Holding Board level including all Steering functions (RM, GPM, BSM) Final sign-off of, for example, 2 to 4 stress scenarios Translating macroeconomic forecasts into risk parameters PDs LGDs Cash Outflows Haircuts etc. Differentiated stress for various individual portfolios, e.g.: Foreign-FX denominated loans Illiquid assets Sensitive products Business sectors etc. Computation of impact on ERSTE Group P&L RWAs Capital Ratios ECap etc. ERM s qualification of results Discussion at Holding Steering Group level Derivation of proposed actions Analysis and discussion of results at Holding Board level (including all Steering functions) Decision on action and targets Design of action plan Identification of countermeasures (e.g. hedging) Review of limits Review of business and risk strategies Change dedication of capital etc. RM: Risk Management GPM: Group Performance Management BSM: Balance Sheet Management ERM: Enterprise-wide Risk Management PD: probability of default LGD: loss given default P&L: profit and loss RWA: risk weighted assets ECap: Economic Capital Execution and implementation of selected measures Capital buffer Limit setting Requirement for contingency plan Forecast of Riskbearing Capacity Calculation etc. 34

35 Agenda 1) Ist die Krise schon vorüber? 2) Was ist Risikomanagement? 3) Warum müssen Banken regulatorisch vorgeschrieben Eigenkapital halten? 4) Welche Folgen haben höhere Eigenkapitalanforderungen? 5) Das Risiko um Staatsanleihen und Liquiditäts- Risikomanagement 6) Welche Rolle erfüllen Stresstests im Risikomanagement? 7) Risikopositionen in der Bilanz am Beispiel der Erste Group 35

36 Income statement (IFRS) FY 2011 performance affected by one-off items in Q3 in EUR million Change Comment Net interest income 5, , % Solid performance of core business Risk provisions for loans (2,266.9) (2,021.0) 12.2% Up in HU, down or flat all other segments Net fee and commission income 1, ,842.5 (3.0%) Reduced securities business Net trading result (62.0%) Written CDS in International Business General administrative expenses (3,850.9) (3,816.8) 0.9% Other operating result (1,589.9) (439.3) >100.0% Goodwill, banking taxes Result from financial instruments - FV 0.3 (6.0) na Result from financial assets - AfS (66.2) 9.2 na Impairment & selling losses Result from financial assets - HtM (27.1) (5.5) >100.0% on peripheral bonds Pre-tax profit/loss (322.2) 1,324.2 na Taxes on income (240.4) (280.9) (14.4%) Net profit/loss for the period (562.6) 1,043.3 na Non-controlling interests (5.0%) Owners of the parent (718.9) na Additional comments for year-on-year comparison: Impairment of goodwill EUR 1,064.6m for RO, HU and Austrian subsidiaries Written CDS (IB) negative impact on trading of EUR 182.6m in 2011 Additional risk provisions of EUR 450m in Hungary for FX conversion and to raise coverage ratio in Q3 Other taxes (mainly Austrian banking tax) increased to EUR 163.5m 36

37 Balance sheet (IFRS) Successful RWA reduction in non-core business in EUR million Dec 11 Dec 10 Change Comment Cash and balances with central banks 9,413 5, % Temporary additional liquidity from LTRO Loans and advances to credit institutions 7,578 12,496 (39.4%) Reduced non-core business Loans and advances to customers 134, , % Increase in AT, SK Risk provisions for loans and advances (7,027) (6,119) 14.8% Driven by Hungary Derivative financial instruments 10,931 8, % Trading assets 5,876 5, % Financial assets - FV 1,813 2,435 (25.5%) Financial assets - AfS 20,245 17, % Basel 3, excess liquidity and deposit Financial assets - HtM 16,074 14, % growth invested (bonds, CEE region) Equity holdings in associates (22.4%) Intangible assets 3,532 4,675 (24.4%) Impairment of goodwill Property and equipment 2,361 2,446 (3.5%) Current tax assets % Deferred tax assets % Assets held for sale % Other assets 3,382 4,626 (26.9%) Total assets 210, , % Risk-weighted assets 114, ,844 (4.9%) Additional comments: RWA were reduced by 4.9% on cut back of non-core activities Financial assets rose yoy as a result of preparatory actions to meet Basel III liquidity requirements as of 2014 (e.g. LCR) and because of investing surplus liquidity in CEE bonds 37

38 Asset quality review New NPL formation declined yoy New NPL formation declined yoy New formation mainly in Hungary (deterioration of corporate and real estate portfolio) and Romania (weak SME business) Qoq: New NPL formation down from EUR 499m in Q3 to EUR 275m in Q4 30% 25% 20% 15% Erste Group: NPL ratio vs NPL coverage 63.9% 61.4% 60.0% 60.6% 61.0% 65% 60% NPL coverage ratio slightly up to 61.0% 10% 7.6% 7.7% 7.9% 8.2% 8.5% 55% Migration trends still mixed While low risk share is increasing and substandard further decreasing, new NPL formation still significant 5% 0% Dec 10 Mar 11 Jun 11 Sep 11 Dec 11 NPL ratio NPL coverage (exc collateral) 50% Customer loans by risk class Quarterly NPL growth (absolute/relative) 100% 80% 60% 40% 20% 0% 7.6% 7.7% 7.9% 8.2% 8.5% 4.6% 4.4% 3.9% 3.3% 3.2% 17.1% 16.5% 17.6% 18.0% 17.2% 70.7% 71.4% 70.6% 70.5% 71.1% in EUR million 1,600 1, % 5 2.4% % % % 275 8% 4% 0% -4% Dec 10 Mar 11 Jun 11 Sep 11 Dec 11 Dec 10 Mar 11 Jun 11 Sep 11 Dec 11 Low risk Management attn Substandard Non-performing NPL growth (absolute) NPL growth (relative) 38

39 Asset quality review Austria, Czech Republic and Slovakia improved, Hungary and Romania still mixed Stable NPL ratio in Austria Slight reduction of NPLs in savings banks Further reduction of CHF loans due to conversion into EUR loans Czech Republic and Slovakia improved Czech Republic: reduction of NPL ratio mainly due to write-offs and NPL sales Slovakia: Healthy demand for new loans; good new booking quality led to increase of low risk category 25% 20% 15% 10% 5% 0% NPL ratios in key segments 22.7% 21.1% 8.0% 5.6% 5.5% 6.4% Austria Czech R Romania Slovakia Hungary GCIB Dec 10 Mar 11 Jun 11 Sep 11 Dec 11 Hungary and Romania remain challenging countries Romania shows diverging development Still rising NPL ratio due to real estate and SME business New loans booked in retail is mainly low risk business Hungary still problematic Local corporate and real estate business drove new NPL formation NPL coverage ratio down due to usage of provisions for FX conversion 100% 80% 60% 40% 20% 0% NPL coverage ratios in key segments (excluding collateral) 61.4% 69.7% 50.1% 79.2% 70.3% Austria Czech R Romania Slovakia Hungary Dec 10 Mar 11 Jun 11 Sep 11 Dec % GCIB 39

40 Status quo Hungary and Romania Operating in a challenging environment - Still fragile economic outlook for Hungary; Banking market is still very challenging - All three major rating agencies downgraded Hungary to non-investment grade IMF-agreement on financial assistance program (EUR 15-20bn) to be expected in H1 2012; agreement would lead to more sustainable economic measures and more stable currency National Bank of Hungary to introduce 2-year variable-rate refinancing credit facility with the aim of supporting lending activity - EBH to reach profitability in 2014 based on its new strategy Focus on local currency lending from locally sourced liquidity; Reduce dependence on parent company funding Smaller size reflects market circumstances 15% headcount reduction, Network reduction by 43 branches GDP growth surprised on the upside in 2011; fiscal reforms and structural adjustments to be continued Real GDP up 2.5% yoy supported by agriculture, industry and exports New government will not deviate from the agreement with the IMF-EC Target 2012: restructuring state-owned enterprises and selling state stakes in energy and transport companies BCR: Results impacted by sluggish loan growth; lower margins and still high provisioning SIF transaction update: 4 SIFs signed binding agreements; By the end of February 2012 EGB share in BCR is 92.3% Still sound efficiency benefiting from economies of scale and strict cost control Strategic aim to build profitable business with core customers, improve asset structure and actively manage capital 40

41 CEE growth potential Twice as high as in Eurozone - Adjusted for cyclical component, CEE countries (apart from Hungary) have twice as high potential growth than the Eurozone (2-4% vs. 1%) in the following two years - Exports and investments will be the main growth drivers - In Hungary, pending reforms of the labor market, unorthodox policy decisions and a relatively high tax burden have an adverse effect on potential growth 6% 5% 4% 3% 2% 1% 0% -1% -2% Greece Portugal Spain Ireland Average growth of potential output (according to the European Commission) Italy Hungary Slovenia Denmark F Euro area UK Netherlands France Finland Belgium Austria Germany Czech Rep. Sweden Romania Slovakia Poland Source: European Commission, Economic Forecasts Autumn

42 Erste Group in 2012 Focus on retail and corporate business in CEE Despite subdued growth outlook for CEE, underlying macroeconomic data in core markets points towards stronger GDP growth than in most other EU countries Austria, Czech Republic and Slovakia are well positioned to weather a potential recession in EU Romania remains on track despite slow economic recovery Hungary: improved market confidence due to planned IMF negotiations Operating result expected to increase slightly in 2012 Despite ongoing reduction in non-core assets Selective loan growth in our core markets Unchanged cost basis Risk costs to decrease as 2011 extraordinary effects expected not to recur EBA capital ratio to exceed 9% beyond 30 June

Taxation in Austria - Keypoints. CONFIDA Klagenfurt Steuerberatungsgesellschaft m.b.h

Taxation in Austria - Keypoints 1 CONFIDA TAX AUDIT CONSULTING Our history: Founded in 1977 Currently about 200 employees Member of International Association of independent accounting firms since1994 Our

Taxation in Austria - Keypoints 1 CONFIDA TAX AUDIT CONSULTING Our history: Founded in 1977 Currently about 200 employees Member of International Association of independent accounting firms since1994 Our

Call Centers and Low Wage Employment in International Comparison

Wissenschaftszentrum Nordrhein-Westfalen Kulturwissenschaftliches Institut Wuppertal Institut für Klima, Umwelt, Energie Institut Arbeit und Technik Call Centers and Low Wage Employment in International

Wissenschaftszentrum Nordrhein-Westfalen Kulturwissenschaftliches Institut Wuppertal Institut für Klima, Umwelt, Energie Institut Arbeit und Technik Call Centers and Low Wage Employment in International

Bankenunion Rekapitalisierung Bad Bank?

Bankenunion Rekapitalisierung Bad Bank? Finanzmarkt Round-Table, Frankfurt, 7. Nov. 2012 Prof. Dr. habil. Manfred Jäger-Ambrożewicz Financial Mathematics & Financial Products Email: Manfred.Jaeger-Ambrozewicz@htw-berlin.de

Bankenunion Rekapitalisierung Bad Bank? Finanzmarkt Round-Table, Frankfurt, 7. Nov. 2012 Prof. Dr. habil. Manfred Jäger-Ambrożewicz Financial Mathematics & Financial Products Email: Manfred.Jaeger-Ambrozewicz@htw-berlin.de

Rechnungswesen Prüfung (30 Minuten - 10 Punkte)

") Rechnungswesen Prüfung (30 Minuten - 10 Punkte) 1/4 - Aktiva Programmelement Verfahrensmethode Zeit Punkte Aktiva Füllen Sie die Leerstellen aus 5' 1.5 Die Aktiven zeigen die Herkunft der Vermögensgegenstände

Rechnungswesen Prüfung (30 Minuten - 10 Punkte) 1/4 - Aktiva Programmelement Verfahrensmethode Zeit Punkte Aktiva Füllen Sie die Leerstellen aus 5' 1.5 Die Aktiven zeigen die Herkunft der Vermögensgegenstände

de Gruyter Textbook Risk Management Bearbeitet von Thomas Wolke

de Gruyter Textbook Risk Management Bearbeitet von Thomas Wolke 1. Auflage 2017. Buch. XVIII, 360 S. Softcover ISBN 978 3 11 044052 2 Format (B x L): 17 x 24 cm Wirtschaft > Management > Risikomanagement

de Gruyter Textbook Risk Management Bearbeitet von Thomas Wolke 1. Auflage 2017. Buch. XVIII, 360 S. Softcover ISBN 978 3 11 044052 2 Format (B x L): 17 x 24 cm Wirtschaft > Management > Risikomanagement

Audi Investor and Analyst Day 2011 Axel Strotbek

Audi Investor and Analyst Day 2011 Axel Strotbek Member of the Board of Management, Finance and Organization Economic development of key sales regions 2007 to [GDP in % compared with previous year] USA

Audi Investor and Analyst Day 2011 Axel Strotbek Member of the Board of Management, Finance and Organization Economic development of key sales regions 2007 to [GDP in % compared with previous year] USA

Überblick Konjunkturindikatoren Eurozone

Überblick Konjunkturindikatoren Eurozone Volkswirtschaftlicher Volkswirtschaftlicher Bereich Bereich Indikator Indikator Wachstum Wachstum Bruttoinlandsprodukt Bruttoinlandsprodukt Inflationsrate, Inflationsrate,

Überblick Konjunkturindikatoren Eurozone Volkswirtschaftlicher Volkswirtschaftlicher Bereich Bereich Indikator Indikator Wachstum Wachstum Bruttoinlandsprodukt Bruttoinlandsprodukt Inflationsrate, Inflationsrate,

Immobilienfinanzierung und Finanzmarkt

1/26 Immobilienfinanzierung und Finanzmarkt Moritz Schularick Frankfurt 4. Mai 2017 University of Bonn; CEPR and CESIfo schularick@uni-bonn.de 2/26 When you combine ignorance and leverage, you get some

1/26 Immobilienfinanzierung und Finanzmarkt Moritz Schularick Frankfurt 4. Mai 2017 University of Bonn; CEPR and CESIfo schularick@uni-bonn.de 2/26 When you combine ignorance and leverage, you get some

Containerschiffahrt Prognosen + Entwicklung Heilbronn, 13. Juli 2010. von Thorsten Kröger NYK Line (Deutschland) GmbH, Hamburg

GmbH, Hamburg") Heilbronn, 13. Juli 2010 von Thorsten Kröger NYK Line (Deutschland) GmbH, Hamburg Agenda Das Krisenjahr 2009 in der Containerschiffahrt Die Konsolidierung sowie Neuausrichtung (2010) Slow Steaming Capacity

Heilbronn, 13. Juli 2010 von Thorsten Kröger NYK Line (Deutschland) GmbH, Hamburg Agenda Das Krisenjahr 2009 in der Containerschiffahrt Die Konsolidierung sowie Neuausrichtung (2010) Slow Steaming Capacity

Aufbau eines IT-Servicekataloges am Fallbeispiel einer Schweizer Bank

SwissICT 2011 am Fallbeispiel einer Schweizer Bank Fritz Kleiner, fritz.kleiner@futureways.ch future ways Agenda Begriffsklärung Funktionen und Aspekte eines IT-Servicekataloges Fallbeispiel eines IT-Servicekataloges

SwissICT 2011 am Fallbeispiel einer Schweizer Bank Fritz Kleiner, fritz.kleiner@futureways.ch future ways Agenda Begriffsklärung Funktionen und Aspekte eines IT-Servicekataloges Fallbeispiel eines IT-Servicekataloges

Women Entrepreneurship in Germany and Access to Capital

Summary Slide Women Entrepreneurship in Germany and Access to Capital Women Entrepreneurship in Germany and Access to Capital Presentation at ESTRAD Lecture Exploring Growth Financing for Women Entrepreneurs,

Summary Slide Women Entrepreneurship in Germany and Access to Capital Women Entrepreneurship in Germany and Access to Capital Presentation at ESTRAD Lecture Exploring Growth Financing for Women Entrepreneurs,

U N D E R S T A N D I N G P E N S I O N A N D E M P L O Y E E B E N E F I T S I N T R A N S A C T I O N S

H E A L T H W E A L T H C A R E E R U N D E R S T A N D I N G P E N S I O N A N D E M P L O Y E E B E N E F I T S I N T R A N S A C T I O N S G E R M A N M & A A N D P R I V A T E E Q U I T Y F O R U M

H E A L T H W E A L T H C A R E E R U N D E R S T A N D I N G P E N S I O N A N D E M P L O Y E E B E N E F I T S I N T R A N S A C T I O N S G E R M A N M & A A N D P R I V A T E E Q U I T Y F O R U M

Providers of climate services in Germany

Providers of climate services in Germany National Dialog Prof. Dr. Maria Manez Costa Dr. Jörg Cortekar 2 Procedure Mapping of climate services providers - Germany Network development between the providers

Providers of climate services in Germany National Dialog Prof. Dr. Maria Manez Costa Dr. Jörg Cortekar 2 Procedure Mapping of climate services providers - Germany Network development between the providers

Labour law and Consumer protection principles usage in non-state pension system

Labour law and Consumer protection principles usage in non-state pension system by Prof. Dr. Heinz-Dietrich Steinmeyer General Remarks In private non state pensions systems usually three actors Employer

Labour law and Consumer protection principles usage in non-state pension system by Prof. Dr. Heinz-Dietrich Steinmeyer General Remarks In private non state pensions systems usually three actors Employer

How to develop and improve the functioning of the audit committee The Auditor s View

How to develop and improve the functioning of the audit committee The Auditor s View May 22, 2013 Helmut Kerschbaumer KPMG Austria Audit Committees in Austria Introduced in 2008, applied since 2009 Audit

How to develop and improve the functioning of the audit committee The Auditor s View May 22, 2013 Helmut Kerschbaumer KPMG Austria Audit Committees in Austria Introduced in 2008, applied since 2009 Audit

Ausbildungsordnung für den EFA European Financial Advisor (in der Fassung vom 07.10.2013)

") Ausbildungsordnung für den EFA European Financial Advisor (in der Fassung vom 07.10.2013) 1 Grundsätze für das Ausbildungswesen... 2 2 Ausbildungsrahmen... 2 3 Weiterbildungsrahmen... 2 4 Abschließende

Ausbildungsordnung für den EFA European Financial Advisor (in der Fassung vom 07.10.2013) 1 Grundsätze für das Ausbildungswesen... 2 2 Ausbildungsrahmen... 2 3 Weiterbildungsrahmen... 2 4 Abschließende

Possible Solutions for Development of Multilevel Pension System in the Republic of Azerbaijan

Possible Solutions for Development of Multilevel Pension System in the Republic of Azerbaijan by Prof. Dr. Heinz-Dietrich Steinmeyer Introduction Multi-level pension systems Different approaches Different

Possible Solutions for Development of Multilevel Pension System in the Republic of Azerbaijan by Prof. Dr. Heinz-Dietrich Steinmeyer Introduction Multi-level pension systems Different approaches Different

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena http://www.im.uni-jena.de Contents I. Learning Objectives II. III. IV. Recap

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena http://www.im.uni-jena.de Contents I. Learning Objectives II. III. IV. Recap

32. Fachtagung der Vermessungsverwaltungen, Trient 2015

32. Fachtagung der Vermessungsverwaltungen, Trient 2015 Taxation of immovable property Dipl.-Ing. Hubert Plainer Content Definitions Legal principles Taxation of immovable properties Non built-up areas

32. Fachtagung der Vermessungsverwaltungen, Trient 2015 Taxation of immovable property Dipl.-Ing. Hubert Plainer Content Definitions Legal principles Taxation of immovable properties Non built-up areas

Energieeffizienz und Erneuerbare Energien Programme der EZ -- ein Zwischenstand

Energieeffizienz und Erneuerbare Energien Programme der EZ -- ein Zwischenstand Climate Policy Capacity Building Seminar Kiew 07.10.04 Klaus Gihr Senior Project Manager Europe Department Was sind unsere

Energieeffizienz und Erneuerbare Energien Programme der EZ -- ein Zwischenstand Climate Policy Capacity Building Seminar Kiew 07.10.04 Klaus Gihr Senior Project Manager Europe Department Was sind unsere

Franke & Bornberg award AachenMünchener private annuity insurance schemes top grades

Franke & Bornberg award private annuity insurance schemes top grades Press Release, December 22, 2009 WUNSCHPOLICE STRATEGIE No. 1 gets best possible grade FFF ( Excellent ) WUNSCHPOLICE conventional annuity

Franke & Bornberg award private annuity insurance schemes top grades Press Release, December 22, 2009 WUNSCHPOLICE STRATEGIE No. 1 gets best possible grade FFF ( Excellent ) WUNSCHPOLICE conventional annuity

AuDiT-Credit Dynamix. Von der Einzelfallbetrachtung zur Portfoliosteuerung. Wien 2014

AuDiT-Credit Dynamix Von der Einzelfallbetrachtung zur Portfoliosteuerung Wien 2014 Zielsetzung des Tools AuDiT Credit Dynamix Bestimmung von inhärenten Kreditrisiken im Portefeuille für Unternehmen und

AuDiT-Credit Dynamix Von der Einzelfallbetrachtung zur Portfoliosteuerung Wien 2014 Zielsetzung des Tools AuDiT Credit Dynamix Bestimmung von inhärenten Kreditrisiken im Portefeuille für Unternehmen und

Cluster policies (in Europe)

") Cluster policies (in Europe) Udo Broll, Technische Universität Dresden, Germany Antonio Roldán-Ponce, Universidad Autónoma de Madrid, Spain & Technische Universität Dresden, Germany 2 Cluster and global

Cluster policies (in Europe) Udo Broll, Technische Universität Dresden, Germany Antonio Roldán-Ponce, Universidad Autónoma de Madrid, Spain & Technische Universität Dresden, Germany 2 Cluster and global

Das Risikomanagement gewinnt verstärkt an Bedeutung

Das Risikomanagement gewinnt verstärkt an Bedeutung 3/9/2009 Durch die internationale, wirtschaftliche Verpflechtung gewinnt das Risikomanagement verstärkt an Bedeutung 2 3/9/2009 Das IBM-Cognos RiskCockpit:

Das Risikomanagement gewinnt verstärkt an Bedeutung 3/9/2009 Durch die internationale, wirtschaftliche Verpflechtung gewinnt das Risikomanagement verstärkt an Bedeutung 2 3/9/2009 Das IBM-Cognos RiskCockpit:

WP2. Communication and Dissemination. Wirtschafts- und Wissenschaftsförderung im Freistaat Thüringen

WP2 Communication and Dissemination Europa Programm Center Im Freistaat Thüringen In Trägerschaft des TIAW e. V. 1 GOALS for WP2: Knowledge information about CHAMPIONS and its content Direct communication

WP2 Communication and Dissemination Europa Programm Center Im Freistaat Thüringen In Trägerschaft des TIAW e. V. 1 GOALS for WP2: Knowledge information about CHAMPIONS and its content Direct communication

Soziale Abgaben und Aufwendungen für Altersversorgung und A054. Soziale Abgaben und Aufwendungen für Altersversorgung und A056

Gewinn- und Verlustrechnung der Banken - Profit and loss account of banks Liste der Variablen - List of Variables Codes Beschreibung Description A000 Aufwendungen insgesamt Total charges A010 Zinsaufwendungen

Gewinn- und Verlustrechnung der Banken - Profit and loss account of banks Liste der Variablen - List of Variables Codes Beschreibung Description A000 Aufwendungen insgesamt Total charges A010 Zinsaufwendungen

Klausur BWL V Investition und Finanzierung (70172)

") Klausur BWL V Investition und Finanzierung (70172) Prof. Dr. Daniel Rösch am 13. Juli 2009, 13.00-14.00 Name, Vorname Anmerkungen: 1. Bei den Rechenaufgaben ist die allgemeine Formel zur Berechnung der

Klausur BWL V Investition und Finanzierung (70172) Prof. Dr. Daniel Rösch am 13. Juli 2009, 13.00-14.00 Name, Vorname Anmerkungen: 1. Bei den Rechenaufgaben ist die allgemeine Formel zur Berechnung der

Satisfactory H results

Investor Presentation Satisfactory H1 2018 results 3 August 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Investor Presentation Satisfactory H1 2018 results 3 August 2018 Árni Ellefsen, CEO Disclaimer This presentation contains statements regarding future results, which are subject to risks and uncertainties.

Mock Exam Behavioral Finance

Mock Exam Behavioral Finance For the following 4 questions you have 60 minutes. You may receive up to 60 points, i.e. on average you should spend about 1 minute per point. Please note: You may use a pocket

Mock Exam Behavioral Finance For the following 4 questions you have 60 minutes. You may receive up to 60 points, i.e. on average you should spend about 1 minute per point. Please note: You may use a pocket

AVL The Thrill of Solutions. Paul Blijham, Wien, 04.07.2005

AVL The Thrill of Solutions Paul Blijham, Wien, 04.07.2005 The Automotive Market and its Importance 58 million vehicles are produced each year worldwide 700 million vehicles are registered on the road

AVL The Thrill of Solutions Paul Blijham, Wien, 04.07.2005 The Automotive Market and its Importance 58 million vehicles are produced each year worldwide 700 million vehicles are registered on the road

Makroökonomische Kreditrisikoprognose Financial Institutions. Wien, 29. April 2014

Makroökonomische Kreditrisikoprognose Financial Institutions Wien, 29. April 2014 CreditDynamix ist ein hochgradig effizientes Kreditrisikosystem welches höchste Transparenz bietet A B C D E Bilanzdaten

Makroökonomische Kreditrisikoprognose Financial Institutions Wien, 29. April 2014 CreditDynamix ist ein hochgradig effizientes Kreditrisikosystem welches höchste Transparenz bietet A B C D E Bilanzdaten

IT Governance im Zusammenspiel mit IT Audit

IT Governance im Zusammenspiel mit IT Audit ISACA After Hours Seminar Nicola Varuolo, Internal Audit AXA AXA Gruppe 52 Millionen Kunden weltweit 79 Milliarden Euro Geschäftsvolumen 150 000 Mitarbeitende

IT Governance im Zusammenspiel mit IT Audit ISACA After Hours Seminar Nicola Varuolo, Internal Audit AXA AXA Gruppe 52 Millionen Kunden weltweit 79 Milliarden Euro Geschäftsvolumen 150 000 Mitarbeitende

German Taxation of Islamic Finance (Sukuk)

") German Taxation of Islamic Finance (Sukuk) Andreas Patzner BaFin Conference on Islamic Finance May 2012 Contents Particulars Slides Islamic Financial Instruments 2 Sukuk (Islamic Bond) 3 Sukuk (Islamic

German Taxation of Islamic Finance (Sukuk) Andreas Patzner BaFin Conference on Islamic Finance May 2012 Contents Particulars Slides Islamic Financial Instruments 2 Sukuk (Islamic Bond) 3 Sukuk (Islamic

Sustainability Balanced Scorecard as a Framework for Eco-Efficiency Analysis

Sustainability Balanced Scorecard as a Framework for Eco-Efficiency Analysis Andreas Möller amoeller@uni-lueneburg.de umweltinformatik.uni-lueneburg.de Stefan Schaltegger schaltegger@uni-lueneburgde www.uni-lueneburg.de/csm

Sustainability Balanced Scorecard as a Framework for Eco-Efficiency Analysis Andreas Möller amoeller@uni-lueneburg.de umweltinformatik.uni-lueneburg.de Stefan Schaltegger schaltegger@uni-lueneburgde www.uni-lueneburg.de/csm

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena http://www.im.uni-jena.de Contents I. Learning Objectives II. III. IV. Recap

Lehrstuhl für Allgemeine BWL Strategisches und Internationales Management Prof. Dr. Mike Geppert Carl-Zeiß-Str. 3 07743 Jena http://www.im.uni-jena.de Contents I. Learning Objectives II. III. IV. Recap

Implicit Public Debt in Social Security and elsewhere or What you see is less than what you have

Implicit Public Debt in Social Security and elsewhere or What you see is less than what you have Prof. Dr. Bernd Raffelhüschen Albert-Ludwigs-University Freiburg, Germany University of Bergen, Norway Lecture

Implicit Public Debt in Social Security and elsewhere or What you see is less than what you have Prof. Dr. Bernd Raffelhüschen Albert-Ludwigs-University Freiburg, Germany University of Bergen, Norway Lecture

Support Technologies based on Bi-Modal Network Analysis. H. Ulrich Hoppe. Virtuelles Arbeiten und Lernen in projektartigen Netzwerken

Support Technologies based on Bi-Modal Network Analysis H. Agenda 1. Network analysis short introduction 2. Supporting the development of virtual organizations 3. Supporting the development of compentences

Support Technologies based on Bi-Modal Network Analysis H. Agenda 1. Network analysis short introduction 2. Supporting the development of virtual organizations 3. Supporting the development of compentences

Investmentprofil der Immobilienfonds von Raiffeisen Investment profile Raiffeisen Real Estate Funds

Investmentprofil der Immobilienfonds von Raiffeisen Investment profile Raiffeisen Real Estate Funds Die aktuelle Investitionsstrategie der Raiffeisen Immobilien KAG The current investment strategy of Raiffeisen

Investmentprofil der Immobilienfonds von Raiffeisen Investment profile Raiffeisen Real Estate Funds Die aktuelle Investitionsstrategie der Raiffeisen Immobilien KAG The current investment strategy of Raiffeisen

An Introduction to Monetary Theory. Rudolf Peto

An Introduction to Monetary Theory Rudolf Peto 0 Copyright 2013 by Prof. Rudolf Peto, Bielefeld (Germany), www.peto-online.net 1 2 Preface This book is mainly a translation of the theoretical part of my

An Introduction to Monetary Theory Rudolf Peto 0 Copyright 2013 by Prof. Rudolf Peto, Bielefeld (Germany), www.peto-online.net 1 2 Preface This book is mainly a translation of the theoretical part of my

Projektrisikomanagement im Corporate Risk Management

VERTRAULICH Projektrisikomanagement im Corporate Risk Management Stefan Friesenecker 24. März 2009 Inhaltsverzeichnis Risikokategorien Projekt-Klassifizierung Gestaltungsdimensionen des Projektrisikomanagementes

VERTRAULICH Projektrisikomanagement im Corporate Risk Management Stefan Friesenecker 24. März 2009 Inhaltsverzeichnis Risikokategorien Projekt-Klassifizierung Gestaltungsdimensionen des Projektrisikomanagementes

Mobility trends in the Baltic Sea Region

Mobility trends in the Baltic Sea Region Conference on promoting strategic and innovative mobility for students and researchers 23 November 2010 in Copenhagen by Dr. Birger Hendriks Outline Forms of mobility

Mobility trends in the Baltic Sea Region Conference on promoting strategic and innovative mobility for students and researchers 23 November 2010 in Copenhagen by Dr. Birger Hendriks Outline Forms of mobility

Oktober 2012: Wirtschaftliche Einschätzung im Euroraum rückläufig, in der EU aber stabil

EUROPÄISCHE KOMMISSION PRESSEMITTEILUNG Brüssel, 30. Oktober 2012 Oktober 2012: Wirtschaftliche Einschätzung im Euroraum rückläufig, in der EU aber stabil Der Indikator der wirtschaftlichen Einschätzung

EUROPÄISCHE KOMMISSION PRESSEMITTEILUNG Brüssel, 30. Oktober 2012 Oktober 2012: Wirtschaftliche Einschätzung im Euroraum rückläufig, in der EU aber stabil Der Indikator der wirtschaftlichen Einschätzung

Japan-EU Free Trade Agreement

Japan-EU Free Trade Agreement Hanns Günther Hilpert Content I. JAPEU: Strategic Importance Public Ignorance? II. Japan-EU: Declining Trade Relationship III. Why a Japan-EU FTA? IV. Difficult To Penetrate

Japan-EU Free Trade Agreement Hanns Günther Hilpert Content I. JAPEU: Strategic Importance Public Ignorance? II. Japan-EU: Declining Trade Relationship III. Why a Japan-EU FTA? IV. Difficult To Penetrate

Results of the Working Table in Bonn, Germany Efficient Office Space Solutions III. Speaker: Robert Erfen

Results of the Working Table in Bonn, Germany Efficient Office Space Solutions III Speaker: Robert Erfen Strategies for cost reduction Calculations & Tools Bundesanstalt für Immobilienaufgaben Seite 2

Results of the Working Table in Bonn, Germany Efficient Office Space Solutions III Speaker: Robert Erfen Strategies for cost reduction Calculations & Tools Bundesanstalt für Immobilienaufgaben Seite 2

Security of Pensions

Security of Pensions by Prof. Dr. Heinz-Dietrich Steinmeyer - Pensions are of essential importance for people and security of pensions important for them for a number of reasons - People depend on pensions

Security of Pensions by Prof. Dr. Heinz-Dietrich Steinmeyer - Pensions are of essential importance for people and security of pensions important for them for a number of reasons - People depend on pensions

Überblick Konjunkturindikatoren Eurozone

Überblick Konjunkturindikatoren Eurozone Volkswirtschaftlicher Bereich Indikator Volkswirtschaftlicher Bereich Indikator Wachstum Bruttoinlandsprodukt Wachstum Bruttoinlandsprodukt Preise Inflationsrate

Überblick Konjunkturindikatoren Eurozone Volkswirtschaftlicher Bereich Indikator Volkswirtschaftlicher Bereich Indikator Wachstum Bruttoinlandsprodukt Wachstum Bruttoinlandsprodukt Preise Inflationsrate

WE SHAPE INDUSTRY 4.0 BOSCH CONNECTED INDUSTRY DR.-ING. STEFAN AßMANN

WE SHAPE INDUSTRY 4.0 BOSCH CONNECTED INDUSTRY DR.-ING. STEFAN AßMANN Bosch-Definition for Industry 4.0 Our Seven Features Connected Manufacturing Connected Logistics Connected Autonomous and Collaborative

WE SHAPE INDUSTRY 4.0 BOSCH CONNECTED INDUSTRY DR.-ING. STEFAN AßMANN Bosch-Definition for Industry 4.0 Our Seven Features Connected Manufacturing Connected Logistics Connected Autonomous and Collaborative

Kapitalmarktunion: was liegt noch auf dem Tisch, insbesondere für die Versicherungswirtschaft?

Kapitalmarktunion: was liegt noch auf dem Tisch, insbesondere für die Versicherungswirtschaft? Prof. Karel Van Hulle KU Leuven Institutional Money: Insurance Day Wien, den 11. September 2018 Kapitalmarktunion:

Kapitalmarktunion: was liegt noch auf dem Tisch, insbesondere für die Versicherungswirtschaft? Prof. Karel Van Hulle KU Leuven Institutional Money: Insurance Day Wien, den 11. September 2018 Kapitalmarktunion:

The Solar Revolution New Ways for Climate Protection with Solar Electricity

www.volker-quaschning.de The Solar Revolution New Ways for Climate Protection with Solar Electricity Hochschule für Technik und Wirtschaft HTW Berlin ECO Summit ECO14 3. June 2014 Berlin Crossroads to

www.volker-quaschning.de The Solar Revolution New Ways for Climate Protection with Solar Electricity Hochschule für Technik und Wirtschaft HTW Berlin ECO Summit ECO14 3. June 2014 Berlin Crossroads to

v+s Output Quelle: Schotter, Microeconomics, , S. 412f

The marginal cost function for a capacity-constrained firm At output levels that are lower than the firm s installed capacity of K, the marginal cost is merely the variable marginal cost of v. At higher

The marginal cost function for a capacity-constrained firm At output levels that are lower than the firm s installed capacity of K, the marginal cost is merely the variable marginal cost of v. At higher

HIR Method & Tools for Fit Gap analysis

HIR Method & Tools for Fit Gap analysis Based on a Powermax APML example 1 Base for all: The Processes HIR-Method for Template Checks, Fit Gap-Analysis, Change-, Quality- & Risk- Management etc. Main processes

HIR Method & Tools for Fit Gap analysis Based on a Powermax APML example 1 Base for all: The Processes HIR-Method for Template Checks, Fit Gap-Analysis, Change-, Quality- & Risk- Management etc. Main processes

Ein- und Zweifamilienhäuser Family homes

Wohnwelten / Living Environments Ein- und Zweifamilienhäuser Family homes Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean Energy

Wohnwelten / Living Environments Ein- und Zweifamilienhäuser Family homes Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean Energy

LRED and Value Chain Promotion

LRED and Value Chain Promotion combining spatial and sectoral perspectives on economic development Andreas Springer-Heinze GTZ Head Office Division Agriculture, Food and Fisheries Abteilung Agrarwirtschaft,

LRED and Value Chain Promotion combining spatial and sectoral perspectives on economic development Andreas Springer-Heinze GTZ Head Office Division Agriculture, Food and Fisheries Abteilung Agrarwirtschaft,

The new IFRS proposal for leases - The initial and subsequent measurement -

Putting leasing on the line: The new IFRS proposal for leases - The initial and subsequent measurement - Martin Vogel 22. May 2009, May Fair Hotel, London 2004 KPMG Deutsche Treuhand-Gesellschaft Aktiengesellschaft

Putting leasing on the line: The new IFRS proposal for leases - The initial and subsequent measurement - Martin Vogel 22. May 2009, May Fair Hotel, London 2004 KPMG Deutsche Treuhand-Gesellschaft Aktiengesellschaft

Dun & Bradstreet Compact Report

Dun & Bradstreet Compact Report Identification & Summary (C) 20XX D&B COPYRIGHT 20XX DUN & BRADSTREET INC. - PROVIDED UNDER CONTRACT FOR THE EXCLUSIVE USE OF SUBSCRIBER 86XXXXXX1. ATTN: Example LTD Identification

Dun & Bradstreet Compact Report Identification & Summary (C) 20XX D&B COPYRIGHT 20XX DUN & BRADSTREET INC. - PROVIDED UNDER CONTRACT FOR THE EXCLUSIVE USE OF SUBSCRIBER 86XXXXXX1. ATTN: Example LTD Identification

Big Data Analytics. Fifth Munich Data Protection Day, March 23, Dr. Stefan Krätschmer, Data Privacy Officer, Europe, IBM

Big Data Analytics Fifth Munich Data Protection Day, March 23, 2017 C Dr. Stefan Krätschmer, Data Privacy Officer, Europe, IBM Big Data Use Cases Customer focused - Targeted advertising / banners - Analysis

Big Data Analytics Fifth Munich Data Protection Day, March 23, 2017 C Dr. Stefan Krätschmer, Data Privacy Officer, Europe, IBM Big Data Use Cases Customer focused - Targeted advertising / banners - Analysis

Critical Chain and Scrum

Critical Chain and Scrum classic meets avant-garde (but who is who?) TOC4U 24.03.2012 Darmstadt Photo: Dan Nernay @ YachtPals.com TOC4U 24.03.2012 Darmstadt Wolfram Müller 20 Jahre Erfahrung aus 530 Projekten

Critical Chain and Scrum classic meets avant-garde (but who is who?) TOC4U 24.03.2012 Darmstadt Photo: Dan Nernay @ YachtPals.com TOC4U 24.03.2012 Darmstadt Wolfram Müller 20 Jahre Erfahrung aus 530 Projekten

Introduction to the ESPON TIA Quick Check. Erich Dallhammer (ÖIR), Roland Gaugitsch (ÖIR)

, Roland Gaugitsch (ÖIR)") Introduction to the Erich Dallhammer (ÖIR), Roland Gaugitsch (ÖIR) Wien, 12 th Dezember 2018 The Challenge EU policy proposals influence development of different regions differently territorial effects

Introduction to the Erich Dallhammer (ÖIR), Roland Gaugitsch (ÖIR) Wien, 12 th Dezember 2018 The Challenge EU policy proposals influence development of different regions differently territorial effects

Reclaim withholding tax on dividends Third country claimants. Financial Services KPMG Germany

Reclaim withholding tax on dividends Third country claimants Financial Services KPMG Germany 2016 Content 1 German Withholding Tax on dividends violates EU-Law 2 Cash refund opportunity 3 Our services

Reclaim withholding tax on dividends Third country claimants Financial Services KPMG Germany 2016 Content 1 German Withholding Tax on dividends violates EU-Law 2 Cash refund opportunity 3 Our services

Vorstellung RWTH Gründerzentrum

Vorstellung RWTH Gründerzentrum Once an idea has been formed, the center for entrepreneurship supports in all areas of the start-up process Overview of team and services Development of a business plan

Vorstellung RWTH Gründerzentrum Once an idea has been formed, the center for entrepreneurship supports in all areas of the start-up process Overview of team and services Development of a business plan

Dienstleistungsmanagement Übung 5

Dienstleistungsmanagement Übung 5 Univ.-Prof. Dr.-Ing. Wolfgang Maass Chair in Economics Information and Service Systems (ISS) Saarland University, Saarbrücken, Germany Besprechung Übungsblatt 4 Slide

Dienstleistungsmanagement Übung 5 Univ.-Prof. Dr.-Ing. Wolfgang Maass Chair in Economics Information and Service Systems (ISS) Saarland University, Saarbrücken, Germany Besprechung Übungsblatt 4 Slide

Internationale Energiewirtschaftstagung TU Wien 2015

Internationale Energiewirtschaftstagung TU Wien 2015 Techno-economic study of measures to increase the flexibility of decentralized cogeneration plants on a German chemical company Luis Plascencia, Dr.

Internationale Energiewirtschaftstagung TU Wien 2015 Techno-economic study of measures to increase the flexibility of decentralized cogeneration plants on a German chemical company Luis Plascencia, Dr.

15. ISACA TrendTalk. Sourcing Governance Audit. C. Koza, 19. November 2014, Audit IT, Erste Group Bank AG

15. ISACA TrendTalk Sourcing Governance Audit C. Koza, 19. November 2014, Audit IT, Erste Group Bank AG Page 1 Agenda IT-Compliance Anforderung für Sourcing Tradeoff between economic benefit and data security

15. ISACA TrendTalk Sourcing Governance Audit C. Koza, 19. November 2014, Audit IT, Erste Group Bank AG Page 1 Agenda IT-Compliance Anforderung für Sourcing Tradeoff between economic benefit and data security

Labor Demand. Anastasiya Shamshur

Labor Demand Anastasiya Shamshur 16.03.2011 Outline Labor Supply Labor Demand always DERIVED: demand for labor is derived from the demand for a rm's output, not the rm's desire fore hire employees. Equilibrium

Labor Demand Anastasiya Shamshur 16.03.2011 Outline Labor Supply Labor Demand always DERIVED: demand for labor is derived from the demand for a rm's output, not the rm's desire fore hire employees. Equilibrium

Carsten Berkau: Bilanzen Solution to Chapter 13

Task IM-13.4: Eigenkapitalveränderungsrechnung (Statement of Changes in Equity along IFRSs) ALDRUP AG is a company based on shares and applies the Company s act in Germany (AktG). ALDRUP AG has been established

Task IM-13.4: Eigenkapitalveränderungsrechnung (Statement of Changes in Equity along IFRSs) ALDRUP AG is a company based on shares and applies the Company s act in Germany (AktG). ALDRUP AG has been established

Economics of Climate Adaptation (ECA) Shaping climate resilient development

Shaping climate resilient development") Economics of Climate Adaptation (ECA) Shaping climate resilient development A framework for decision-making Dr. David N. Bresch, david_bresch@swissre.com, Andreas Spiegel, andreas_spiegel@swissre.com Klimaanpassung

Economics of Climate Adaptation (ECA) Shaping climate resilient development A framework for decision-making Dr. David N. Bresch, david_bresch@swissre.com, Andreas Spiegel, andreas_spiegel@swissre.com Klimaanpassung

Triparty-Repo Die Geldmarktalternative

Triparty-Repo Die Geldmarktalternative Behrad Hasheminia Treasury Deutsche Börse Group Tel: +49 69 211 18256 E-mail: behrad.hasheminia@deutsche-boerse.com Carsten Hiller Sales Manager Global Securities

Triparty-Repo Die Geldmarktalternative Behrad Hasheminia Treasury Deutsche Börse Group Tel: +49 69 211 18256 E-mail: behrad.hasheminia@deutsche-boerse.com Carsten Hiller Sales Manager Global Securities

Elektronische Identifikation und Vertrauensdienste für Europa

Brüssel/Berlin Elektronische Identifikation und Vertrauensdienste für Europa Wir wären dann soweit --- oder? Thomas Walloschke Director EMEIA Security Technology Office eidas REGULATION No 910/2014 0 eidas

Brüssel/Berlin Elektronische Identifikation und Vertrauensdienste für Europa Wir wären dann soweit --- oder? Thomas Walloschke Director EMEIA Security Technology Office eidas REGULATION No 910/2014 0 eidas

Makroökonomie I: Vorlesung # 10 Geld und die Geldnachfrage

Makroökonomie I: Vorlesung # 10 Geld und die Geldnachfrage 1 Vorlesung Nr #10 1. Was ist Geld? Ein Exkurs 2. Die Definition von Geld nach Jevons... 3.... und aus moderner Sicht 4. Die Geldnachfrage 5.

Makroökonomie I: Vorlesung # 10 Geld und die Geldnachfrage 1 Vorlesung Nr #10 1. Was ist Geld? Ein Exkurs 2. Die Definition von Geld nach Jevons... 3.... und aus moderner Sicht 4. Die Geldnachfrage 5.

Turbulente Zeiten wohin steuert die Wirtschaft? Prof. Dr. Klaus W. Wellershoff

Turbulente Zeiten wohin steuert die Wirtschaft? Prof. Dr. Klaus W. Wellershoff Baden, 18. November 2014 Welt: BIP Wachstumsraten Industrienationen und BRIC-Staaten im Vergleich Seite 2 Welt: BIP Wachstumsraten

Turbulente Zeiten wohin steuert die Wirtschaft? Prof. Dr. Klaus W. Wellershoff Baden, 18. November 2014 Welt: BIP Wachstumsraten Industrienationen und BRIC-Staaten im Vergleich Seite 2 Welt: BIP Wachstumsraten

FIVNAT-CH. Annual report 2002

FIVNAT-CH Schweizerische Gesellschaft für Reproduktionsmedizin Annual report 2002 Date of analysis 15.01.2004 Source: FileMaker Pro files FIVNAT_CYC.FP5 and FIVNAT_PAT.FP5 SUMMARY TABLE SUMMARY RESULTS

FIVNAT-CH Schweizerische Gesellschaft für Reproduktionsmedizin Annual report 2002 Date of analysis 15.01.2004 Source: FileMaker Pro files FIVNAT_CYC.FP5 and FIVNAT_PAT.FP5 SUMMARY TABLE SUMMARY RESULTS

Introduction Classified Ad Models Capital Markets Day Berlin, December 10, 2014. Dr Andreas Wiele, President Marketing and Classified Ad Models

Capital Markets Day Berlin, December 10, 2014 Dr Andreas Wiele, President Marketing and Classified Ad Models Axel Springer s transformation to digital along core areas of expertise 3 Zimmer mit Haus im

Capital Markets Day Berlin, December 10, 2014 Dr Andreas Wiele, President Marketing and Classified Ad Models Axel Springer s transformation to digital along core areas of expertise 3 Zimmer mit Haus im

Exercise (Part II) Anastasia Mochalova, Lehrstuhl für ABWL und Wirtschaftsinformatik, Kath. Universität Eichstätt-Ingolstadt 1

Anastasia Mochalova, Lehrstuhl für ABWL und Wirtschaftsinformatik, Kath. Universität Eichstätt-Ingolstadt 1") Exercise (Part II) Notes: The exercise is based on Microsoft Dynamics CRM Online. For all screenshots: Copyright Microsoft Corporation. The sign ## is you personal number to be used in all exercises. All

Exercise (Part II) Notes: The exercise is based on Microsoft Dynamics CRM Online. For all screenshots: Copyright Microsoft Corporation. The sign ## is you personal number to be used in all exercises. All

Energieeffizienz im internationalen Vergleich

Energieeffizienz im internationalen Vergleich Miranda A. Schreurs Sachverständigenrat für Umweltfragen (SRU) Forschungszentrum für Umweltpolitik (FFU), Freie Universität Berlin Carbon Dioxide Emissions

Energieeffizienz im internationalen Vergleich Miranda A. Schreurs Sachverständigenrat für Umweltfragen (SRU) Forschungszentrum für Umweltpolitik (FFU), Freie Universität Berlin Carbon Dioxide Emissions

Customer-specific software for autonomous driving and driver assistance (ADAS)

") This press release is approved for publication. Press Release Chemnitz, February 6 th, 2014 Customer-specific software for autonomous driving and driver assistance (ADAS) With the new product line Baselabs

This press release is approved for publication. Press Release Chemnitz, February 6 th, 2014 Customer-specific software for autonomous driving and driver assistance (ADAS) With the new product line Baselabs

Transparente Geschäftsberichterstattung Pflicht oder Kür?

Geschäftsberichte Symposium 2014 Transparente Geschäftsberichterstattung Pflicht oder Kür? Sandra Schreiner Head Group External Reporting 12. Juni 2014 Transparente Geschäftsberichterstattung Grundsatz

Geschäftsberichte Symposium 2014 Transparente Geschäftsberichterstattung Pflicht oder Kür? Sandra Schreiner Head Group External Reporting 12. Juni 2014 Transparente Geschäftsberichterstattung Grundsatz

Die Vollendung von Basel III oder schon Basel IV?

Die Vollendung von Basel III oder schon Basel IV? Pressegespräch des Bankenverbandes Dr. Michael Kemmer Hauptgeschäftsführer und Mitglied des Vorstands Ort: Frankfurt am Main Datum: 25.1.2016 Die Regulierer

Die Vollendung von Basel III oder schon Basel IV? Pressegespräch des Bankenverbandes Dr. Michael Kemmer Hauptgeschäftsführer und Mitglied des Vorstands Ort: Frankfurt am Main Datum: 25.1.2016 Die Regulierer

Report Date 30.06.2015 Report Currency

EN Bank Kommunalkredit Austria AG Report Date 30.06.2015 Report Currency EUR Public Pfandbrief or Public Covered Bond (fundierte Bankschuldverschreibung) 1. OVERVIEW CRD/ UCITS compliant Ja Share of ECB

EN Bank Kommunalkredit Austria AG Report Date 30.06.2015 Report Currency EUR Public Pfandbrief or Public Covered Bond (fundierte Bankschuldverschreibung) 1. OVERVIEW CRD/ UCITS compliant Ja Share of ECB

Handwerk Trades. Arbeitswelten / Working Environments. Green Technology for the Blue Planet Clean Energy from Solar and Windows

Arbeitswelten / Working Environments Handwerk Trades Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean Energy from Solar and Windows

Arbeitswelten / Working Environments Handwerk Trades Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean Energy from Solar and Windows

Danish Horticulture a long history!

Danish Association of Horticultural Producers Danish Association of Horticultural Producers The National Centre acts as a development and support unit for the. The 46 local advisory centres sell advice

Danish Association of Horticultural Producers Danish Association of Horticultural Producers The National Centre acts as a development and support unit for the. The 46 local advisory centres sell advice

Übersicht. Zinskurve Technische Rückstellung. Martin Hahn 2

QIS 6 LTG Maßnahmen Übersicht Extrapolation der maßgeblichen risikofreien Zinskurve Volatility Adjustment (Volatilitätsanpassung) Matching Adjustment (Matching-Anpassung) Transitional Measures (Übergangsbestimmungen)

QIS 6 LTG Maßnahmen Übersicht Extrapolation der maßgeblichen risikofreien Zinskurve Volatility Adjustment (Volatilitätsanpassung) Matching Adjustment (Matching-Anpassung) Transitional Measures (Übergangsbestimmungen)

THE NEW ERA. nugg.ad ist ein Unternehmen von Deutsche Post DHL

nugg.ad EUROPE S AUDIENCE EXPERTS. THE NEW ERA THE NEW ERA BIG DATA DEFINITION WHAT ABOUT MARKETING WHAT ABOUT MARKETING 91% of senior corporate marketers believe that successful brands use customer data

nugg.ad EUROPE S AUDIENCE EXPERTS. THE NEW ERA THE NEW ERA BIG DATA DEFINITION WHAT ABOUT MARKETING WHAT ABOUT MARKETING 91% of senior corporate marketers believe that successful brands use customer data

Einkommensaufbau mit FFI:

For English Explanation, go to page 4. Einkommensaufbau mit FFI: 1) Binäre Cycle: Eine Position ist wie ein Business-Center. Ihr Business-Center hat zwei Teams. Jedes mal, wenn eines der Teams 300 Punkte

For English Explanation, go to page 4. Einkommensaufbau mit FFI: 1) Binäre Cycle: Eine Position ist wie ein Business-Center. Ihr Business-Center hat zwei Teams. Jedes mal, wenn eines der Teams 300 Punkte

prorm Budget Planning promx GmbH Nordring Nuremberg

prorm Budget Planning Budget Planning Business promx GmbH Nordring 100 909 Nuremberg E-Mail: support@promx.net Content WHAT IS THE prorm BUDGET PLANNING? prorm Budget Planning Overview THE ADVANTAGES OF

prorm Budget Planning Budget Planning Business promx GmbH Nordring 100 909 Nuremberg E-Mail: support@promx.net Content WHAT IS THE prorm BUDGET PLANNING? prorm Budget Planning Overview THE ADVANTAGES OF

Corporate Digital Learning, How to Get It Right. Learning Café

0 Corporate Digital Learning, How to Get It Right Learning Café Online Educa Berlin, 3 December 2015 Key Questions 1 1. 1. What is the unique proposition of digital learning? 2. 2. What is the right digital

0 Corporate Digital Learning, How to Get It Right Learning Café Online Educa Berlin, 3 December 2015 Key Questions 1 1. 1. What is the unique proposition of digital learning? 2. 2. What is the right digital

Renditequellen der Anlagemärkte

Renditequellen der Anlagemärkte Analyse von Risikoprämien empirische Erkenntnisse PPCmetrics AG Dr. Diego Liechti, Senior Consultant Zürich, 13. Dezember 2013 Inhalt Einführung Aktienrisikoprämie Weitere

Renditequellen der Anlagemärkte Analyse von Risikoprämien empirische Erkenntnisse PPCmetrics AG Dr. Diego Liechti, Senior Consultant Zürich, 13. Dezember 2013 Inhalt Einführung Aktienrisikoprämie Weitere

Produzierendes Gewerbe Industrial production

Arbeitswelten / Working Environments Produzierendes Gewerbe Industrial production Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean

Arbeitswelten / Working Environments Produzierendes Gewerbe Industrial production Grüne Technologie für den Blauen Planeten Saubere Energie aus Solar und Fenstern Green Technology for the Blue Planet Clean

ZWEIRAD-INDUSTRIE-VERBAND E. V. (The German Bicycle Industry Association)

") Friedrichshafen, 28/08/2012 The Biking Trend Continues to Strengthen Information from the ZIV on the First Half of 2012 Press Release ZWEIRAD-INDUSTRIE-VERBAND E. V. (The German Bicycle Industry Association)

Friedrichshafen, 28/08/2012 The Biking Trend Continues to Strengthen Information from the ZIV on the First Half of 2012 Press Release ZWEIRAD-INDUSTRIE-VERBAND E. V. (The German Bicycle Industry Association)

European Qualification Strategies in Information and Communications Technology (ICT)

") European Qualification Strategies in Information and Communications Technology (ICT) Towards a European (reference) ICT Skills and Qualification Framework Results and Recommendations from the Leornardo-da-Vinci-II

European Qualification Strategies in Information and Communications Technology (ICT) Towards a European (reference) ICT Skills and Qualification Framework Results and Recommendations from the Leornardo-da-Vinci-II

Connecting the dots on Germany s Energiewende and its impact on European energy policy

Connecting the dots on Germany s Energiewende and its impact on European energy policy Rebecca Bertram Heinrich Böll Foundation Heinrich-Böll-Stiftung Schumannstraße 8 Telefon 030.285 34-0 Die grüne politische

Connecting the dots on Germany s Energiewende and its impact on European energy policy Rebecca Bertram Heinrich Böll Foundation Heinrich-Böll-Stiftung Schumannstraße 8 Telefon 030.285 34-0 Die grüne politische

Copyright by Max Weishaupt GmbH, D Schwendi

Improving Energy Efficiency through Burner Retrofit Overview Typical Boiler Plant Cost Factors Biggest Efficiency Losses in a boiler system Radiation Losses Incomplete Combustion Blowdown Stack Losses

Improving Energy Efficiency through Burner Retrofit Overview Typical Boiler Plant Cost Factors Biggest Efficiency Losses in a boiler system Radiation Losses Incomplete Combustion Blowdown Stack Losses

Less is more? Checks and balances in sport organisations

Less is more? Checks and balances in sport organisations Dr. Michael Groll Play the Game Conference Aarhus, October 29th 2013 Checks and Balances in Sport Organisations Insufficient democratic participatio

Less is more? Checks and balances in sport organisations Dr. Michael Groll Play the Game Conference Aarhus, October 29th 2013 Checks and Balances in Sport Organisations Insufficient democratic participatio

Finanzierung betriebsspezifischer vs. allgemeiner Qualifizierung

4.4.2 (1) Finanzierung betriebsspezifischer vs. allgemeiner Qualifizierung Expected annual earnings Post-training level of output D A 1 X 3 B G 2 E C Marginal product in job B Marginal product in job A

4.4.2 (1) Finanzierung betriebsspezifischer vs. allgemeiner Qualifizierung Expected annual earnings Post-training level of output D A 1 X 3 B G 2 E C Marginal product in job B Marginal product in job A

Financial Intelligence

Financial Intelligence Financial Literacy Dr. Thomas Ernst, Hewlett-Packard GmbH Welche Unternehmenskennzahlen gibt es? Was bedeuten sie? Wie kommen sie zustande? Wie hängen sie zusammen? Welche Rolle

Financial Intelligence Financial Literacy Dr. Thomas Ernst, Hewlett-Packard GmbH Welche Unternehmenskennzahlen gibt es? Was bedeuten sie? Wie kommen sie zustande? Wie hängen sie zusammen? Welche Rolle

Veröffentlichung einer Mitteilung nach 27a Abs. 1 WpHG

Veröffentlichung einer Mitteilung nach 27a Abs. 1 WpHG Peter-Behrens-Str. 15 12459 Berlin First Sensor-Aktie ISIN DE0007201907 Ι WKN 720190 21. August 2014 Veröffentlichung gemäß 26 Abs. 1 WpHG mit dem

Veröffentlichung einer Mitteilung nach 27a Abs. 1 WpHG Peter-Behrens-Str. 15 12459 Berlin First Sensor-Aktie ISIN DE0007201907 Ι WKN 720190 21. August 2014 Veröffentlichung gemäß 26 Abs. 1 WpHG mit dem

Lessons learned VC Investment Erfahrungen

Lessons learned VC Investment Erfahrungen Venture Capital Club München, 24.10.2007 Bernd Seibel General Partner Agenda Key TVM Capital information Investorenkreis Gesellschafterkreis Investment Konditionen

Lessons learned VC Investment Erfahrungen Venture Capital Club München, 24.10.2007 Bernd Seibel General Partner Agenda Key TVM Capital information Investorenkreis Gesellschafterkreis Investment Konditionen

Outline. 5. A Chance for Entrepreneurs? Porter s focus strategy and the long tail concept. 6. Discussion. Prof. Dr. Anne König, Germany, 27. 08.

Mass Customized Printed Products A Chance for Designers and Entrepreneurs? Burgdorf, 27. 08. Beuth Hochschule für Technik Berlin Prof. Dr. Anne König Outline 1. Definitions 2. E-Commerce: The Revolution

Mass Customized Printed Products A Chance for Designers and Entrepreneurs? Burgdorf, 27. 08. Beuth Hochschule für Technik Berlin Prof. Dr. Anne König Outline 1. Definitions 2. E-Commerce: The Revolution

Prozesse als strategischer Treiber einer SOA - Ein Bericht aus der Praxis

E-Gov Fokus Geschäftsprozesse und SOA 31. August 2007 Prozesse als strategischer Treiber einer SOA - Ein Bericht aus der Praxis Der Vortrag zeigt anhand von Fallbeispielen auf, wie sich SOA durch die Kombination

E-Gov Fokus Geschäftsprozesse und SOA 31. August 2007 Prozesse als strategischer Treiber einer SOA - Ein Bericht aus der Praxis Der Vortrag zeigt anhand von Fallbeispielen auf, wie sich SOA durch die Kombination

KNORR VENTURE CAPITAL GROUP, INC. FINANCIAL STATEMENTS ********************************************* DECEMBER 31, 2003

KNORR VENTURE CAPITAL GROUP, INC. FINANCIAL STATEMENTS ********************************************* DECEMBER 31, 2003 Claude Todoroff CPA, Inc. Certified Public Accountant 4707 Scott St. - Torrance, Ca.

KNORR VENTURE CAPITAL GROUP, INC. FINANCIAL STATEMENTS ********************************************* DECEMBER 31, 2003 Claude Todoroff CPA, Inc. Certified Public Accountant 4707 Scott St. - Torrance, Ca.